The Problem Disguised As The Solution: Warren Buffett

We need a fair economic system, not the generosity of billionaires

The opinions expressed here are those of the author alone and do not represent the views of any associated entities.

Warren Buffett is beloved by many. Known as “The Oracle of Omaha” by his fans, he is often referred to as “the greatest investor of all time”. Indeed, the performance of his company, Berkshire Hataway, has been stellar.

Although, in recent times he seems to have lost his touch. Berkshire Hathaway has outperformed the S&P 500 just 11 times in the last 20 years.

Despite his mediocre investment results over the last couple of decades, he is still revered because he comes across as a “good” billionaire.

Buffett has admitted that it’s not right for wealthy individuals like himself to pay lower tax rates than regular folks like his secretary. He went so far as to write a now famous op-ed in the New York Times, Stop Coddling the Super-Rich, advocating for higher taxes on the wealthy.

You almost never hear anything negative about him in the media.

”The 92-year-old has received $100,000 a year since 1980, a fraction of the $18 million average pay of S&P 500 CEOs in 2021. … he doesn't spend much: he lives in a modest family home, drives a basic car, and eats breakfast at McDonald's.”

He has even promised to give away 99% of his wealth to charity.

Buffett’s persona of a loveable, altruistic grandpa makes it more palatable that he has amassed a fortune of over $100 billion, making him the fifth richest person in the world. To put this sum in context, consider that $100 billion USD is enough to buy 200,000 Canadian houses at the current average price of around $700k CAD. Here is an interesting visualization of extraordinary levels of wealth like Buffett’s.

Unlike other billionaires like Musk or Zuckerberg, Buffett doesn’t have many haters. He seems like a nice guy who is on our side. We believe that if we are smart with our money like he is, and purchase shares in solid companies like Berkshire Hathaway, we can all get rich alongside him.

Buffett is often quoted in the media commenting on financial markets; investors hang on to his every word, hoping to get a leg up from his insights. His annual letter to shareholders is highly anticipated each year. This year’s edition caused quite a stir due to controversial comments on stock buybacks, otherwise known as share repurchases.

Buffett's defense of share repurchases comes against a backdrop of growing skepticism towards the practice.

Last year the US attempted to discourage share repurchases by instituting a 1% tax on them. Joe Biden has recently started pushing the idea of increasing the tax rate to 4%. Canada announced a similar tax of 2% that will take effect in 2024.

What is a share repurchase anyways?

Profits generated by corporations can be used in a few different ways. They can be put towards lowering prices, to the benefit of customers. Employees can be rewarded through higher wages. Investments can be made to upgrade technology or infrastructure, improving future prospects for the company. Or, profits can be paid out to shareholders, usually through dividends or share repurchases.

During a share repurchase, a company distributes profits to shareholders by buying back previously issued shares.

Shareholders who sell their shares are able to cash out at a good price due to the extra demand created by the repurchase. Shareholders who hold onto their shares end up with a bigger stake in the company since there are fewer shares of the company in existence after the repurchase.

Share repurchases are preferred to dividends for a variety of (mostly tax-related) reasons; they have become the dominant method of distributing profits to shareholders.

If you’re looking for some more details, here’s a nice infographic that describes share repurchases in more detail.

In the US, share repurchases were illegal up until 1982

They were illegal in part because of their susceptibility to abuse.

The Atlantic did a great story a few years back detailing how Craig Menear, the former CEO (and current Chairman) of Home Depot, used company profits to enrich himself through share repurchases:

Astronomical sums are going towards repurchasing shares

US firms spent $1.26 trillion USD buying back stocks in 2023. Unfortunately, it’s not easy to come up with a similar high-level estimate of share repurchases in Canada because of poor financial reporting regulations. However, given the close ties between our two economies, it’s probably fair to assume that corporate spending trends are similar North of the border. There are clear examples of the dominance of share repurchases in Canada: Loblaws typically spends over a billion dollars annually repurchasing shares, and the amount is growing each year.

It’s hard to conceptualize these large dollar values. Most people can’t imagine a billion, nevermind a trillion, of anything. So let’s put things in simpler terms with the help of a 2018 report from The National Employment Law Project and The Roosevelt Institute:

McDonald’s could pay all of its 1.9 million workers almost $4,000 more a year if the company redirected the money it spends on buybacks to workers’ paychecks instead.

If Starbucks reallocated money from share repurchases to compensation, every worker could get a $7,000 raise.

With the money currently spent on buybacks, Lowe’s, CVS, and Home Depot could give each of their workers raises of at least $18,000 a year.

Similarly, my calculations show that Loblaws could be paying all of its employees thousands of dollars more per year with the money it spends on buybacks.

With this in mind, it becomes clear why incomes haven’t risen in decades; most of the money our economy creates is being used to repurchase shares to the benefit of (primarily wealthy) shareholders.

A lack of competition enables massive share repurchases

I recently read The Boat People, a heart-wrenching story that vividly describes the difficulties endured by the Tamil people fleeing ethnic persecution in Sri Lanka. Midway through the story, a man tries to sell some of his late wife’s jewelry to raise enough funds to secure a trip out of the country. Many people had already escaped his war-torn town, and only one jeweler remained. With no other option, he is forced to sell the jewels to this jeweler for only a fraction of what he knows they are worth.

In this example, the customer gets a bad price because there was no competition in the market. You can bet that the jeweler wasn’t paying their employees well either, since no other employers were around to offer alternative jobs.

We find ourselves in an analogous scenario outside of this story.

It is well documented that due to decades of weak antitrust law (also known as competition law in Canada) enforcement, most sectors in both the Canadian and US economies are dominated by at best a handful of firms, and at worst, a single company. These companies are able to charge customers as much as they want and pay employees as little as they please since there is nowhere else to turn. The resultant extraordinary profits - made at the expense of customers and employees - are then distributed to shareholders through share repurchases.

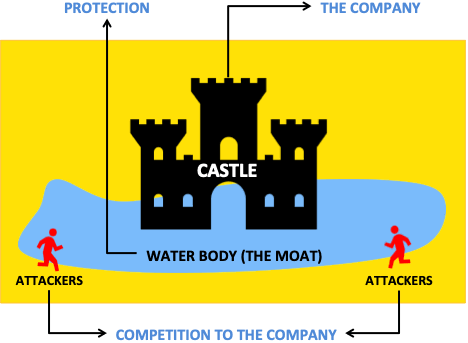

Buffett loves monopolies

Here’s how he characterizes his investment strategy:

What Buffett means is that he likes businesses that are operating in a space where they won’t face competition due to some barrier to entry: the moat. This terminology is just a polite way of describing monopolies.

His affection for monopolies is reflected in the holdings of Berkshire Hathaway, which owns or has owned shares in well-known monopolies like Amazon, Apple, and John Deere, as well as lesser-known firms like DaVita, one of two dialysis companies, and Teva Pharmaceuticals, a manufacturer of generic opioid-based products.

Berkshire Hathaway makes tremendous profits each year by investing in monopolies that prioritize shareholders over customers and employees. Buffett uses these profits to reward Berkshire Hathaway shareholders by repurchasing shares.

Berkshire bought back a total of $27.1 billion worth of shares in 2021. Instead, Berkshire’s subsidiaries could have used this money to pay their employees more, or charge their customers less. Buffett is the largest shareholder of Berkshire, making him the biggest beneficiary of these share repurchases. You don’t end up with $100 billion from a $100k salary, that’s just good publicity. It’s no wonder he is so protective of share repurchases…

Share repurchases disproportionately benefit the ultra-wealthy

Buffett maintains that anyone who says that repurchases are harmful to shareholders or to the country, or particularly beneficial to CEOs, is either an economic illiterate or a silver-tongued demagogue.

I hope the evidence I’ve laid out here explains why he is wrong.

Most of the profits generated by our economy, the fruits of all our labor, are distributed to shareholders through share repurchases. Of course, share repurchases don’t harm shareholders, but that’s not the problem. The issue is that our economic system prioritizes the interests of shareholders over those of customers and employees.

The wealthiest 10% of Americans own 89% of stocks. Stock ownership data for Canada is not as easily accessible, but from what I’ve seen, the distribution in Canada might even be more extreme. For example, a single person, Galen Weston, owns 25% of Loblaws, a company that has immense control over our supply of food.

Shareholders are the main beneficiaries of share repurchases, and the wealthy own more shares. This means that we effectively prioritize the wealthy over the masses. If Buffett doesn’t think this is harmful to a country, he must have a strange conception of what harmful means.

We don’t need “wealthy saviors”

Buffett claims that he thinks “huge dynastic wealth is not desirable for our society.” An ironic claim from someone hoarding so much wealth. We look past these sorts of incongruencies, giving him the benefit of the doubt because he has promised to give the majority of his wealth away. His so-called generosity obscures the fact that the world would be in less need of charity if Buffett, and other investors like him, hadn’t been able to accumulate so much wealth in the first place.

Stronger antitrust law enforcement over the last few decades would have promoted competition that would have prevented many of the companies Buffett has invested in from becoming so profitable. Lower profits would have meant less money going to enriching shareholders through share repurchases. Instead, employees would have been earning higher wages, and customers would have been paying lower prices.

While taxing share repurchases is a step in the right direction, it only treats a symptom. The real disease is monopoly power. Fortunately, the world is starting to recognize this problem. A global movement in antitrust law enforcement has started - Canada needs to join it to stand a chance at building a better future for all Canadians, not just the wealthy.

That’s all for this time.

I would love to hear any thoughts, comments, or concerns you might have about all of this. Feel free to reach out!

Thanks for reading,

Kareem

Officially a subscriber and enjoyed the article. But you haven’t convinced me that buybacks are bad for society!

I think your article rightfully highlights that corporate profits are well above historic norms (currently at 11%+ of US GDP vs. 7% historically), which has translated to wealth accumulation for business owners. I think it also rightfully calls out management abuse of share buybacks for personal benefit (which is also bad for shareholders). However, I disagree with the blanket attack on share buybacks. Share buybacks and dividends are just a mechanism for distributing corporate profits (which is your fundamental concern). They can create value for ongoing shareholders if shares are repurchased below fair value; they can also destroy value for ongoing shareholders if shares are repurchased above fair value (think of any company that bought back shares last year). I think the argument would be stronger to focus on your view of excessive corporate profits vs. share buybacks (a release valve for corporate profits).